Norwegian Cruise Line: Time To Buy

Editor’s note: Seeking Alpha is proud to welcome Josh Germino as a new contributor. It’s easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to the SA PRO archive. Click here to find out more »

Perched for Success

Norwegian Cruise Line (NCLH) is well positioned to outperform the market and its peer group over the next six months. Why? It has been growing organically and continue to do so in light of more and more people taking luxurious, yet affordable cruises on the back of a strong economy. It has posted accelerating, double-digit growth on both its top and bottom line, while investing its cash into more ships. Best of all, the rapid growth is under priced on an absolute and a relative basis, creating an excellent buying opportunity.

Market Outlook

There are a few reasons investors should be optimistic from an economic point of view. First, the market for cruises is growing. Global leisure travel spending from 2017 to 2022 is expected to grow at 5% each year across the globe. Given Norwegian’s physical maneuverability, it has the ability to travel wherever demand arises for its product. Since discretionary spending benefits from low unemployment, demand for cruises has seen steady increases, which has been further bolstered by simpler travel planning and an expanding middle and traveling class.

Secondly, cruise lines account for about 8% of global leisure spending, leaving plenty of room for increased market penetration. CEO Frank Del Rio made an excellent point during his investor day presentation that Norwegian does not necessarily need to steal business from its competitors Royal Caribbean Cruise (RCL) and Carnival Cruise Line (CCL), but rather capture more market share from the travel industry as a whole. This, in my view, gives it two fronts on which to grow its business.

From an economic standpoint, the US economy is chugging along, which should continue to help its cause. Del Rio reiterated that, “Every year, the industry has enjoyed consistent year-over-year growth in cruise passengers no matter what the headwinds are, be they geopolitical events or economic downturns” (Investor Day Presentation). The economy is showing no signs of weakness at the moment and my investment horizon of six months should fall well within this bull market. Also considering that US revenue accounts for 47% of the total, NCLH benefits significantly from a strong macro environment, particularly low unemployment and an appreciating dollar.

The cruise line industry has particularly high barriers to entry which Del Rio estimates to be $700mm to $1b. Aside from its direct competitors of Carnival and Royal Caribbean, they are relatively insulated from being undercut by newcomers.

Secular Trends

An important secular trend which Norwegian taps into is that of purchasing experiences rather than things. Del Rio highlights that “we’ve now shifted away from accumulating stuff to accumulating experiences and you’re going to see more and more people shift their spend, their discretionary spend from accumulating more stuff into experiences and that’s going to benefit the cruise industry in a big, big way” (Investor Day Presentation). Additionally, increased retirement rates of baby boomers should contribute in a meaningful way given they still control the majority of wealth in the US. As a result, that retirement spending will be injected back into circulation, and likely toward discretionary areas such as vacations.

Worth noting is China’s position as the largest outbound tourism market in the world. NCLH is currently trying to tap into China’s leisure market where cruise lines only account for ~1% of leisure spending. If it can successfully tap or create demand, it will work wonders for revenue growth. Currently, China accounts for about 7% of NCLH’s revenue which will increase as it gains more pricing power consequent of limited capacity.

Valuation

Relative to historical market multiples, the stock is plainly undervalued. It currently trades at 15x earnings which is barely above five-year lows, but if a standard 17x market multiple were applied to NCLH it would generate a ~$80.00 price tag, or 52% upside as of 6/7/18 (on a forward earnings basis). Also note, the market is currently trading at 22x earnings, further emphasizing its disparity from fair value. The market has largely ignored the previous four earnings reports which all beat estimates, yet the stock has tumbled from its 52-week high of $61 to as low as $49. This price decline over the past year has been true across its competitors as well, at least in part vindicating the dip from any company specific issues over that period.

Now for the exciting stuff. Norwegian has shown substantial growth in both its top (18.8% CAGR) and bottom line (35.5% CAGR) over the past five years as well as EPS growth of 28.6% annually over that period. Best of all, those numbers have been accelerating with the strongest growth occurring in 2016 and 2017. Free cash flow has grown in tandem (17.7% CAGR) which creates the case to justify its similarly growing debt profile (I’ll get into that later). Built into its free cash flow numbers are substantial capital expenditures with the most recent being the purchase of six new ships (due to arrive incrementally between 2019 and 2025). NCLH has a notably low PEG of 0.5 which seems remarkably cheap given its robust growth over recent years. I posit the market will realize this and price it accordingly over the next six months. The following sensitivity chart gives a good feel for how the earnings growth and multiple expansion can drive the stock price. Forward earnings are currently set at $4.68, per FactSet. Again, that would bring the price to about $80 with the multiple expanding between 16x and 17x.

As Norwegian has gotten larger, so have its margins. Economies of scale have kicked in as it uses its size to leverage more efficiency across operations. It has doubled its net margin from 7.4% to 14.1% in only five years. That’s efficiency. Moreover, management continues to increase its reinvestment of capital into a larger fleet. As mentioned, it has six new ships currently being built and has the youngest fleet among its competitors, an important factor in attracting new customers.

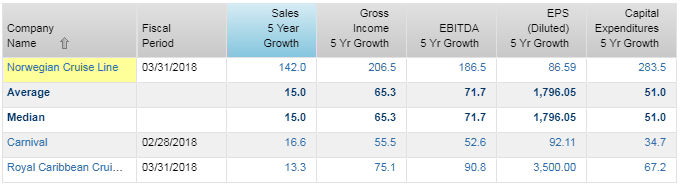

Relative to its industry it is also undervalued on almost every fundamental metric. Of particular note is, once again, PEG (0.4) in comparison to its peer group. The far right column below shows Norwegian relative to peers. Not only is NCLH priced attractively on standard valuation metrics of P/E, P/book, P/CF, and EV/EBITDA, but it also comes with growth that none of the other industry leaders are exhibiting. And since growth has only really accelerated in the past two years or so, it allows you to enter before valuations revert to the market norm or exceed a comfortable buying range.

{kind=link}

Source: FactSet

Technical

On a technical basis, the stock has been trendless for about a year. In my opinion it seems like the stock is taking a metaphorical “breather” after a large run up from late ’16 through ’17. This seems to be a consolidation period combined with some investor profit taking which leads me to believe the stock remains well perched to resume its upward trend. RSI readings, momentum and MACD indicators are consistent with the trendless phase, showing a slight decline over the past six months. This provides a good entry point.

Seasonality

On average, cruise lines tend to outperform the market in the back half of the calendar year. According to a report from JPMorgan, “By quarter, (cruise lines) underperformed the SPX on average by 1% and 3% in the 1Q and 2Q, and outperformed by 5% and 7% in the 3Q and 4Q” (PDF file). July and October have been historically strong months from NCLH where it has not seen a loss notched during those periods for the last five years. From a consumer perspective, it’s logical that more cruises would be booked in the fall or winter months than in the summer months. It seems that investor sentiment follows the same pattern of purchasing stock during stereotypical vacation seasons and selling around spring time. Despite this, Norwegian’s revenue is spread out fairly evenly across all four quarters without any large swings from season to season.

Risks

Of note is the company’s debt. While using it to finance the purchase of six new ships, it’s sporting a 58% debt/cap ratio. Its balance sheet currently holds about $5.6 billion in outstanding, long-term debt, but it generated $1.5 billion in EBITDA during the last fiscal year. The leverage ratio as defined by long-term debt/EBITDA would be about ~3.6x, which is not ideal, but also not catastrophic. It would be susceptible to rising rates in the US, but more so in Europe where most of its variable rate debt is denominated. Norwegian has done an excellent job financing its latest ship purchase with fixed rates at approximately 1.25% and mature 12 years after delivery. FCF covers annual interest expense 1.32x, so it can service its debt, but I wouldn’t expect any dividends soon. Hopefully, growing cash flow will allow the company to attack that debt more aggressively going forward, and if it does, expect the P/E multiple to start expanding. Additionally, rising oil prices have been a concern over the past six months since fuel is an important input for cruise ships. Recent talk of increased supply from OPEC as well as an outright request from the US seems to at least have halted oil’s run up. Come year end, OPEC will stop incrementally decreasing output as it has been doing and readdress whether to increase supply in the wake of concerns in Venezuela and Iran. Nevertheless, it is an important variable to keep an eye on and was definitely a contributor to a flat/decreasing NCLH stock price over the past year.

Conclusion

This stock is in excellent condition for a major run-up. The market has disregarded positive earnings over the past year, leading the stock to drop unfairly. As a result, a good buying opportunity has now presented itself. Backed by a steadily growing US and global economy, I believe NCLH presents an inexpensive option to buy a robust growth profile that has been largely overlooked.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Leave a Reply